Mortgage interest rates play a significant role in homeownership, influencing how much you’ll pay for your dream home over time. But what are mortgage interest rates in 2025, and why should you care? In this article, we’ll explore everything you need to know in a simple, conversational tone—no financial jargon here. Let’s dive in!

Table of Contents

| Sr# | Headings |

|---|---|

| 1 | Introduction to Mortgage Interest Rates |

| 2 | Why Do Mortgage Rates Matter? |

| 3 | What Influences Mortgage Rates in 2025? |

| 4 | Types of Mortgage Interest Rates |

| 5 | Fixed vs. Adjustable-Rate Mortgages |

| 6 | Current Trends in Mortgage Rates |

| 7 | How Global Events Impact Rates |

| 8 | Tips for Securing the Best Rates |

| 9 | How Rates Affect Monthly Payments |

| 10 | Predictions for Mortgage Rates in 2025 |

| 11 | Should You Lock Your Rate Now? |

| 12 | Refinancing in 2025: Is It Worth It? |

| 13 | Common Mistakes to Avoid |

| 14 | Tools to Calculate Mortgage Payments |

| 15 | Conclusion and Final Thoughts |

1. Introduction to Mortgage Interest Rates

A mortgage interest rate is the cost of borrowing money to buy a home. Think of it as the price you pay for the privilege of turning that dream house into your own. It’s usually expressed as a percentage and can make a huge difference in how much you pay over the life of your loan.

2. Why Do Mortgage Rates Matter?

Why should you care about these rates? Well, they determine your monthly payment and overall cost of your loan. For example, even a 1% difference in rates can save or cost you thousands of dollars over time. Imagine it as the “fuel” that powers your home-buying journey—the cheaper the fuel, the further your budget will stretch.

3. What Influences Mortgage Rates in 2025?

Mortgage rates don’t just appear out of thin air. Several factors come into play:

- Economic Conditions: Inflation and unemployment can drive rates up or down.

- Federal Reserve Policies: Decisions by the Fed on interest rates ripple through to mortgages.

- Market Demand: If more people want mortgages, rates may rise.

- Credit Scores: Your personal financial health influences the rate you’re offered.

4. Types of Mortgage Interest Rates

There are two primary types of mortgage interest rates:

- Fixed-Rate Mortgages: These have a steady rate throughout the loan term.

- Adjustable-Rate Mortgages (ARMs): These start with a lower rate that adjusts periodically based on market conditions.

5. Fixed vs. Adjustable-Rate Mortgages

Which is better, fixed or adjustable? It depends on your financial goals and how long you plan to stay in your home:

- Fixed-Rate Pros: Stability and predictability.

- Fixed-Rate Cons: Usually higher initial rates.

- ARM Pros: Lower initial rates.

- ARM Cons: Risk of increasing payments over time.

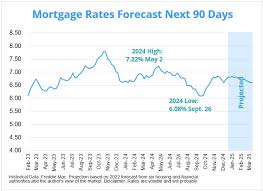

6. Current Trends in Mortgage Rates

As of 2025, mortgage rates have shown a slight increase compared to previous years. However, they remain lower than historical highs. This trend is influenced by ongoing global economic recovery and changes in monetary policies.

7. How Global Events Impact Rates

Did you know that events halfway across the globe can affect your mortgage rate? For instance, geopolitical tensions, trade policies, and international economic shifts often create ripples that impact financial markets, including mortgages.

8. Tips for Securing the Best Rates

Getting the best rate isn’t just about luck; it’s about strategy:

- Improve Your Credit Score: Pay off debts and avoid late payments.

- Save for a Larger Down Payment: More equity can mean a better rate.

- Shop Around: Compare offers from multiple lenders.

9. How Rates Affect Monthly Payments

Here’s a simple breakdown: Higher rates mean higher monthly payments. For example, a $300,000 loan at 4% interest will cost less per month than the same loan at 6%. Use online mortgage calculators to see how rates impact your budget.

10. Predictions for Mortgage Rates in 2025

Experts predict that rates may continue to hover around current levels, with minor fluctuations depending on economic conditions. Staying informed is crucial for timing your purchase or refinance.

11. Should You Lock Your Rate Now?

If rates are trending upward, locking in your rate can protect you from future increases. However, if rates seem likely to drop, it might be worth waiting. It’s a bit like deciding when to buy airline tickets—timing is everything.

12. Refinancing in 2025: Is It Worth It?

Refinancing can help you save money by securing a lower rate or changing your loan terms. Consider it if:

- Current rates are significantly lower than your existing rate.

- You plan to stay in your home long enough to recoup closing costs.

13. Common Mistakes to Avoid

Here are some pitfalls to watch out for:

- Ignoring Fees: Focus on the APR, not just the interest rate.

- Not Shopping Around: The first offer isn’t always the best.

- Skipping Preapproval: Know your budget before house hunting.

14. Tools to Calculate Mortgage Payments

Online calculators are your best friend for estimating payments. They allow you to input loan amount, interest rate, and term to see how everything adds up.

15. Conclusion and Final Thoughts

Understanding what mortgage interest rates in 2025 are and how they work can save you thousands and help you make smarter financial decisions. By staying informed and proactive, you can turn the tide in your favor and achieve your homeownership dreams.